How To Pay A Financial Advisor

Financial advisors don’t work for free and their compensation model is cleverly designed for their benefit, rather than yours.

Fee structure

An asset under management (“AUM”) fee is the most common structure to pay a financial advisor. The advisor charges a percentage of the client assets being managed, typically in the range of 1% per year. In the past, a commission-based model was more common but the industry has de-emphasized that approach in favor of the AUM model.

A less common fee structure is where the advisor charges either a flat fee or an hourly rate. This is similar to other professional services but it has two drawbacks from the advisor’s standpoint:

- it is less profitable than an AUM fee

- the size of the fees are more visible to the client

Understandably, most financial advisors don’t offer this option.

Conflicts

The AUM compensation model may conflict with the client’s best interest. I’ll explain:

1. The client and advisor’s needs can be mis-aligned.

Imagine the client has $500,000 of assets under management . The client asks for advice about paying off a $200,000 mortgage by drawing down some of those assets. If the client does so, the advisor’s fees will decline by 40%. This can be an awkward situation if the advisor counsels against paying off the mortgage.

2. Larger portfolios don’t warrant a proportionally larger fee.

Does a $1 million portfolio require double the fee of a $500,000 account? Surely not. The effort is essentially identical.

3. Bond returns leave little room to pay a fee.

We are in an era of very low interest rates. A portion of your investment portfolio will almost certainly be invested in bonds where the after-tax returns are now less than 2%. With a 1% AUM fee, you keep less than half of the 2% investment gain — more than half accrues to your advisor!

You contribute 100% of the capital, absorb 100% of any losses, but keep less than 50% of the gains. That seems imbalanced. This is particularly important for older clients who typically have a larger proportion of their portfolio invested in bonds.

Remember that the advisor takes no risk and is paid whether portfolio grows or shrinks, or under-performs what could have been achieved by investing in low-cost index funds.

From the advisor’s standpoint, the AUM model has a big advantage — the fees are hidden. Clients often neither know how they compensate their advisor nor how much, and some even think the service is free. These fees do not appear on a monthly invoice but instead are automatically deducted and may require forensic accounting expertise to uncover on an account statement. It’s easy for advisors to avoid a conversation about them.

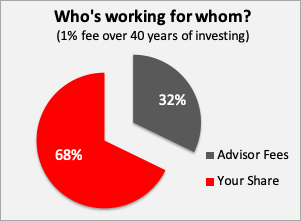

How expensive is a 1% fee?

It sounds insignificant but the optical illusion belies the truth. Here’s the cost of a 1% fee over 40 years:

After 40 years of savings, you’ve given up nearly one-third of the wealth that you otherwise would have accumulated. No one is more clever than the financial services industry in how they extract these hidden fees. You’ll never know it happened.

What should you do?

An hourly rate or fixed fee is your best option. Your fees will be lower and the cost will be transparent. Unsurprisingly, many advisors are unwilling to provide their services on that basis. Even some clients are reluctant because it may seem that the fees are higher because they’re now visible and explicit.

When you seek financial guidance, hire an advisor as you would any other professional service. Your therapist, dentist, and car mechanic don’t charge based on how large your bank account is; why should your financial advisor?

PS: To learn more about what financial advisors actually do and how they add value to their clients, click here.