2019: A Good Year For… Stocks And Bonds

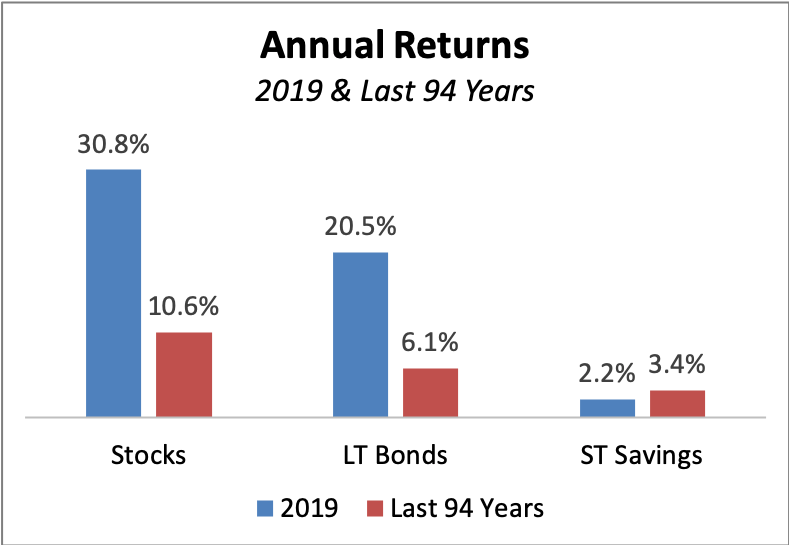

Stocks and bonds generated near-record returns in 2019 — 31% for US stocks and 21% for long-term bonds. If your IRA or 401K was not up a lot in 2019, you were doing something wrong. You’d have to travel back to 1995 to find a year in which stock and bond returns both exceeded these numbers.

Accurate records go back to 1926 and since then, average annual returns have been:

- stocks: 11%

- long-term bonds: 6%

- short-term savings: 3% (think bank CDs, money market funds, or Treasury Bills)

For visual thinkers, here’s a picture of these investment returns:

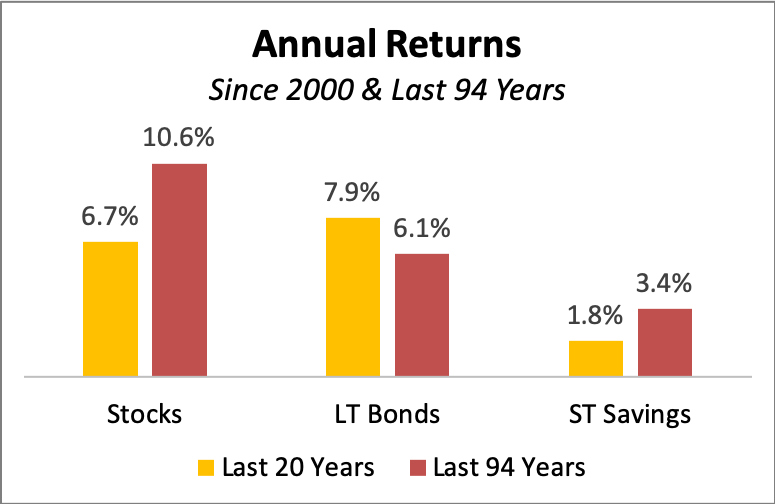

Over the last 20 years, the story is a bit different. Bonds have performed quite well but stocks have fallen short of their historical average:

For stocks, it’s a tale of two decades. The “aught” years of the early 2000s were a terrible time for stocks — first, we had the so-called dot-com crash and then the existential financial crisis of 2008 soon followed, resulting in a flat returns for the decade. After 2008, stocks recovered and it’s been near record performance since then.

Long-term bonds do well when interest rates decline and rates have been doing that for the past 20+ years. In contrast, short-term savings suffer as interest rates decline. And this is what occurred — high returns for long-term bonds and record low returns for short-term savings.

Here’s another view of investment returns in the 21st century:

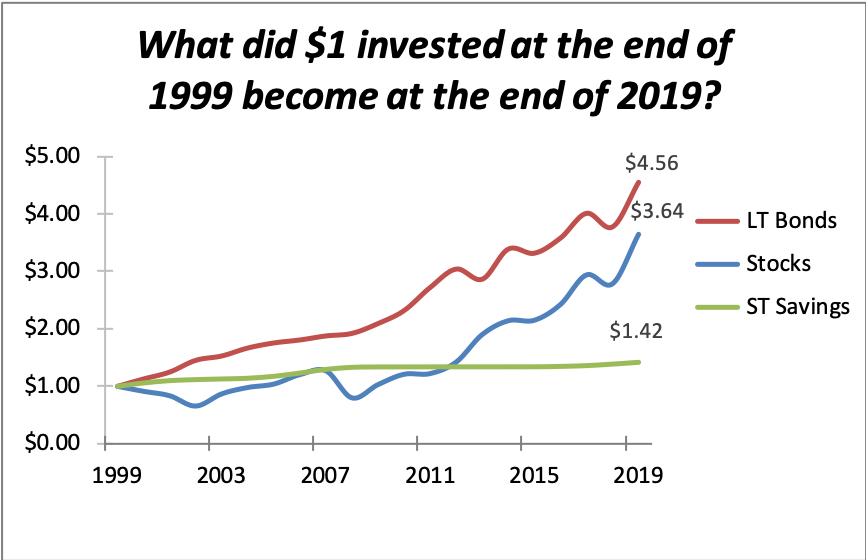

One conclusion from these charts is that short-term savings have never been good investments over the long run.

Yes, you sleep better at night but you pay a price in lower long-term returns. From the last chart, you can see that even with the sub-par returns of stocks in these past 20 years, investing in stocks would have given you nearly triple the returns of bank CDs. That’s a big difference.

What does this all mean for the future? I have no idea (but no one does).

However, one truism has been that the good times for stocks and bonds never last forever. In the next post, I’ll focus on understanding the risks in these investments and why it is psychologically challenging to move your money from that bank CD into stocks and bonds.