Give yourself some credit

Credit reports and credit scores play important roles in our financial lives. What are they and why do they matter?

1. What is credit report?

It’s a dossier of your credit history compiled by a credit bureau. It includes bill and loan payments, status of outstanding debts, inquiries made about new credit applications, and public records such as legal judgments, foreclosures, bankruptcies, etc. Negative information (e.g., missed payments, defaults) typically remains on the report for seven years.

Your credit score is generated from this information.

2. What is a credit score?

It’s a single number that represents your creditworthiness — i.e., a measure of your likelihood of repaying your obligations in full and on time. There are various models but generally, scores range from 300 to 850. Roughly speaking, the qualitative values are:

- excellent: > 750

- fair to good: 650 – 750

- poor: < 650

Excellent credit scores give you the easiest and lowest cost access to credit. Consumers with poor scores are sometimes known as “sub-prime borrowers” and if they are able to secure credit at all, they may pay higher interest rates, incur additional fees, need larger down payments, or require a co-signer. If you need to borrow money, you’ll want to ensure your score is as high as can be.

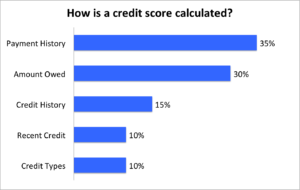

3. How is your score determined?

The specific algorithm these three credit bureaus use is as secretive as the Coca Cola recipe but, also similar to Coke, it’s not much of a secret.

They consider these five factors:

The two most important considerations are:

- Do you have a history of consistently paying your bills in full and on time?

- How much have you borrowed, relative to your borrowing limits?

It is harder for younger adults to generate an excellent credit score simply because they don’t have a long enough payment history.

4. Who calculates them?

There are three consumer-based credit bureaus in the US:

- Equifax

- TransUnion

- Experian

They operate similarly but have their own nuances for what they collect and how they tweak their credit scoring algorithm.

5. Can you check your credit report?

Consumers are entitled to view each of their three credit reports once per year for free. These three companies sponsor a website, annualcreditreport.com, where you can request all three. You are not entitled to a free credit score but some financial institutions and services such as creditkarma.com will provide you with close estimates.

I recommend you check your credit reports occasionally to learn what they know about you and verify if your information is accurate. They each offer a process to contact them to correct errors. Good luck with that.

6. Why should you care?

Your credit score directly affects your ability to do any consumer borrowing — mortgage, car loan or lease, credit card, etc. — and the interest rate you will incur. However, even if you are not looking to borrow money, your credit score can affect other aspects of your life:

- Apartment rentals. A landlord will almost certainly run a credit check on you and this will influence their assessment of you as a potential tenant. You may be rejected or need a co-signer if your credit check returns a poor result.

- Insurance premiums. Automobile and homeowner’s insurance can be influenced by your credit score as it can indirectly signal your likelihood of filing a future claim.

- Employment. Certain employers may request a credit check on new applicants. This may seem unfair but there is nothing to stop them from asking for your permission to do so.

7. How can you improve your score?

The process to improve your score is straightforward but it won’t happen overnight.

- Have bills or loan payments in your name. This could include: credit cards, utilities, car loans, mortgages, student loans, etc. Debit card payments do not count.

- Pay all your bills in full and on time. For credit cards, that means making at least the minimum payment (but see my next point).

- Pay down existing revolving loan balances such as credit cards and home equity loans. You want your “utilization” (the percentage of your available credit that you’re currently using) to be low and decreasing, rather than high and increasing.

- Limit the number of “hard inquiries” that are made to your credit files. These occur when potential lenders make a credit check because you’ve applied for some sort of credit or loan. This is a signal that you’re interested in increasing your borrowing.